Last week, three of the largest banks (JP Morgan Chase, Bank of America and Wells Fargo) released their Q3 earnings reports. In them, we see a glimpse of what’s in store for the economy in the coming months.

“Let’s do the numbers…”

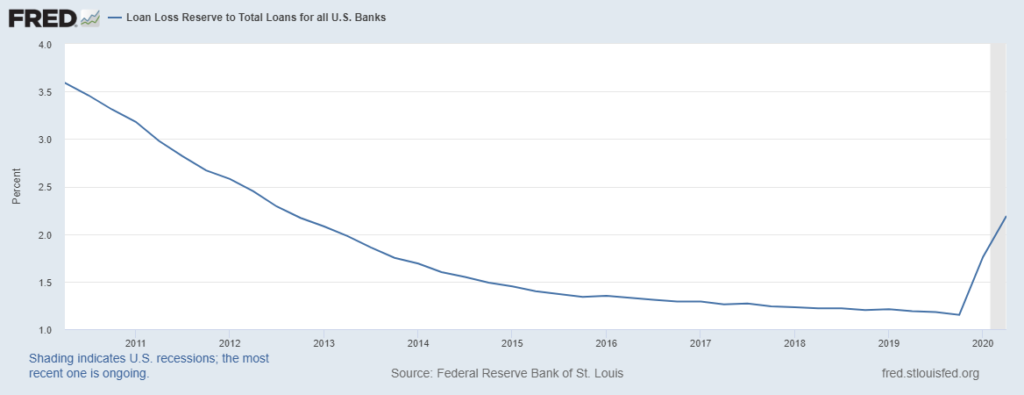

All three banks significantly increased their loan loss reserves earlier in the year, expecting the fallout from the Covid-induced economic shutdown. In Q3, the loan losses did not actually take place. In fact, the actual losses were down significantly from Q2 and the previous year. Chase’s losses were down 94% from Q2, BofA’s were down $.2B and Wells’ were down 38%. That’s great news right?

Yes and no. The banks added to their loan loss reserves, with the notable exception of Chase, which reduced theirs by $600 million. Analysts explained their reduction as over-reserving in previous quarters rather than as a sign of reduced exposure to actual loss. So while not actually having losses is good, no one is releasing reserves, which means they expect to need them in the near future.

What does it mean?

Beginning in the spring, a wave of forbearance took place to avoid huge losses as consumers and businesses were unable to generate the revenue needed to service debt. The recent earnings reports still reflect the benefit of this move since loans in forbearance are not considered non-performing (Wells Fargo’s non-performing assets increased 5%).

The problem is that at some point, these loans must return to normal status, which means the borrowers must have the ability to start making normal payments again. Today, these loans are a huge potential avalanche of bad debt waiting to happen. In fact, Wells Fargo said it best:

“customer forbearance and payment deferral activities instituted in response to the COVID-19 pandemic could delay the recognition of net charge-offs, delinquencies, and nonaccrual status for those customers who would have otherwise moved into past due or nonaccrual status.”

Winners and losers

I shared an article last month on the “winners and losers” created by the current loan forbearance situation. Borrowers are taking the money from skipped loan payments (rents, mortgages, student loans etc.) and instead are buying furniture, hot tubs, making home improvements and paying off debts. At some point, the loans will have to be repaid and the day of reckoning will be here.

All three banks expect loan losses to increase. Chase says otherwise, but their large loss reserve speaks louder than words. When will this happen? Many feel it will be in the next 2 quarters once the election is behind us, the PPP money flushes out of the system and the can can’t be kicked down the road again.

When this happens, banks of all kinds will have to re-grade their loan portfolios and many will no longer be “pass credits”. It hasn’t happened yet, but it’s coming.

Recent Comments